Hurun 2026: China’s unicorn pace doubles in 12 months

Hurun’s 2026 Global Unicorn Index counts 1,603 private companies worth at least $1B. AI value now runs roughly triple fintech’s. China added 80 new entries in 12 months

Global count reaches 1,603 unicorns across 52 countries and 299 cities. The US holds 50.3%.

AI nearly ties fintech in unicorn count (215 vs 216), but holds roughly 3x the aggregate value.

China added 80 new unicorns, one every five days, doubling last year’s pace.

Hard tech now dominates China’s mix, led by semiconductors, AI, life sciences, new energy, and robotics.

Sichuan added three new entries in electric vertical takeoff and landing aircraft (eVTOL), drones, and solar polysilicon.

The Hurun Research Institute released its 2026 Global Unicorn Index on June 25. Valuations are dated January 1, 2026 and updated for material changes ahead of publication. The list tracks non-listed companies founded after 2000 and valued at $1B or above. The index excludes companies that have gone public or been acquired, counting only those still privately held as of the cutoff date.

AI displaces fintech as the dominant value pool

According to Hurun, AI now accounts for 215 unicorns globally and fintech 216. The two sectors are roughly tied by count.

The valuation gap is wider. AI unicorns hold combined value running roughly 3x that of fintech. Hurun chairman Rupert Hoogewerf characterized the shift as a move from fintech transactions toward AI platforms.

The global top 10 by valuation reflects that tilt. Anthropic ranks first, followed by OpenAI, ByteDance, Stripe, Databricks, Ant Group, Revolut, Binance, Shein, and Anduril. Three of the top 10 are Chinese: ByteDance at third, Ant Group at sixth, and Shein at ninth.

US leads with 806 unicorns, China second at 381

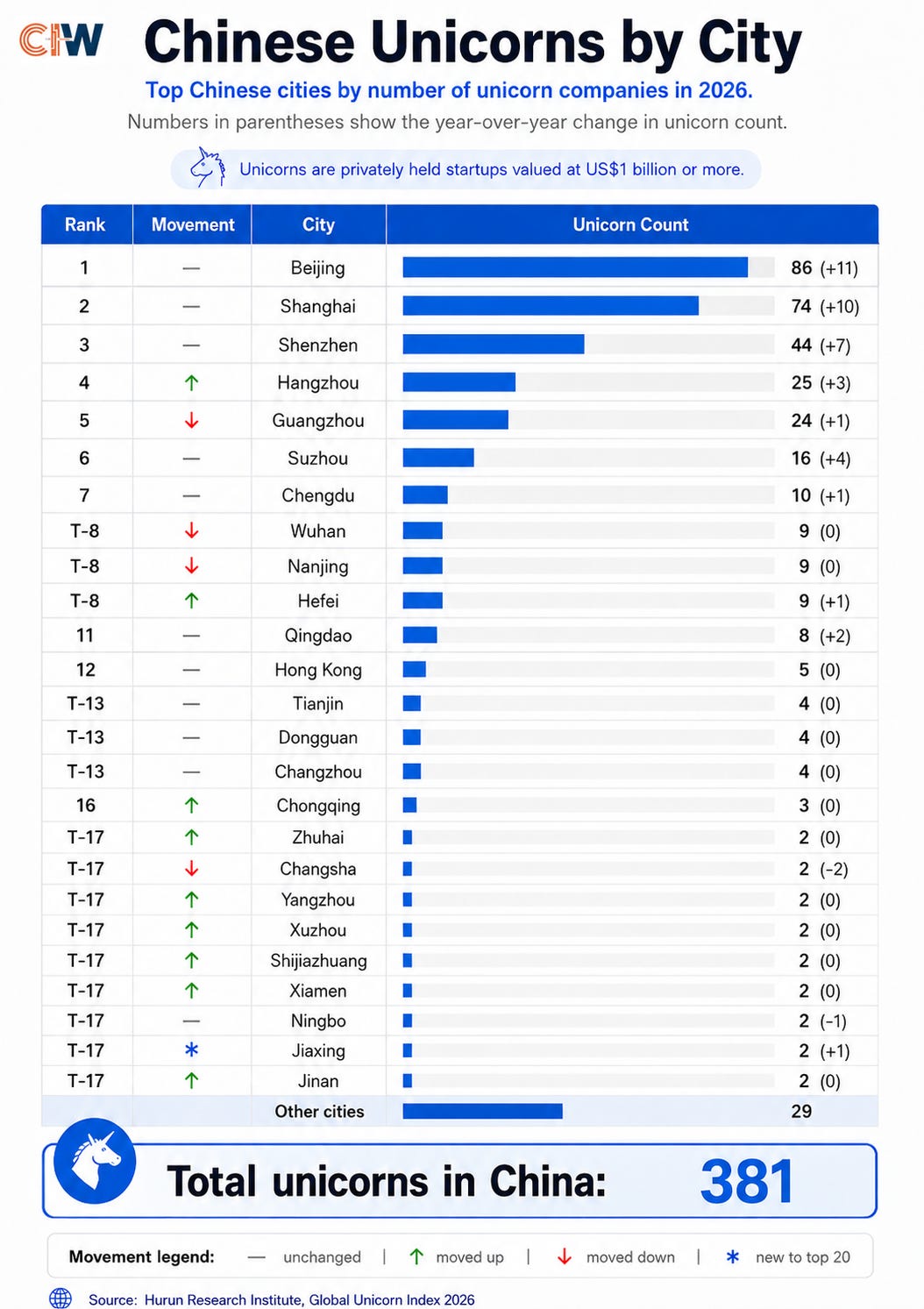

The United States hosts 806 unicorns, up 48 from last year, or 50.3% of the global total. China is second with 381, up 38. The United Kingdom holds 70, India 61, and Germany 31.

San Francisco retains the title of global unicorn capital with 222 unicorns, up 23 from last year. New York follows at 141. Beijing, Shanghai, and London round out the top five at 86, 74, and 60.

China’s creation pace doubles in a year

China added 80 new unicorns this cycle, averaging one every five days. The prior year’s pace was one every 10 days. Hurun projects China’s total could pass 500 within five years if the trend holds.

The net change of 38 is smaller than gross additions of 80. The gap reflects exits through IPO, acquisition, valuation cuts, and reclassification. Net growth still outpaces every market except the US.

Semiconductors and AI lead China’s sector mix

China’s five largest unicorn sectors are semiconductors, AI, life sciences, new energy, and robotics. The composition tilts toward hard tech and capital-intensive industries. Consumer internet plays no longer dominate net adds.

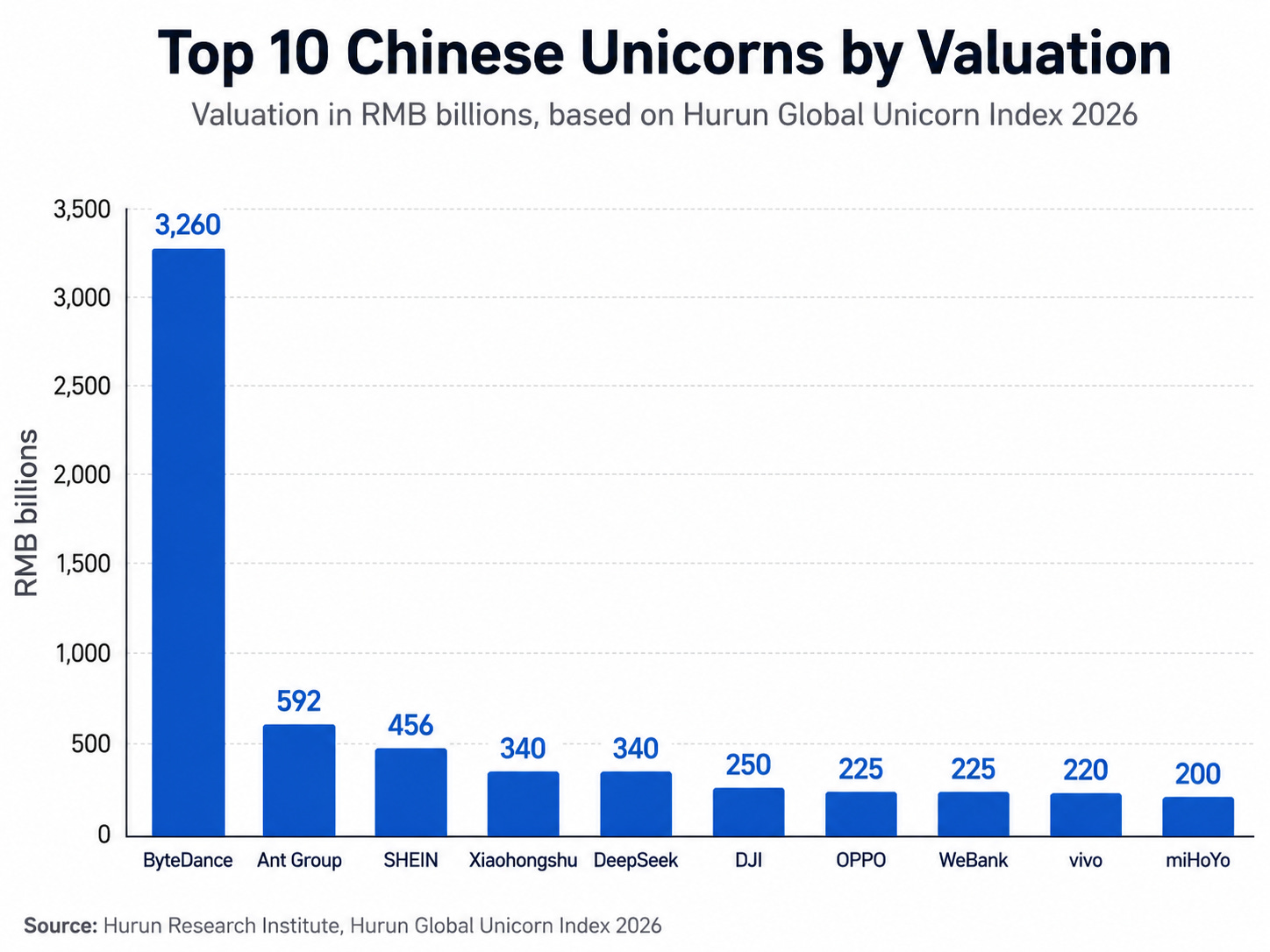

China’s 10 largest unicorns by valuation are ByteDance, Ant Group, Shein, Xiaohongshu, DeepSeek, DJI, Oppo, WeBank, Vivo, and miHoYo. The list spans short video, payments, fast fashion, social commerce, AI foundation models, drones, smartphones, banking, and gaming.

Innovation capital disperses beyond first-tier cities

Beijing leads Chinese cities with 86 unicorns. Shanghai has 74, Shenzhen 44, Hangzhou 25, Guangzhou 24, and Suzhou 16. Chengdu sits seventh with 10.

Wuhan, Nanjing, and Hefei each have 9 unicorns. The trailing tier suggests innovation capital is gradually moving beyond the four first-tier cities into provincial capitals and Yangtze River Delta hubs.

Sichuan’s new entries map to national policy priorities

Sichuan added three names to the list this year: Aerofugia, Tengdun, and Yongxiang. All three sit in central-government priority areas named in recent industrial policy.

Aerofugia develops electric vertical takeoff and landing aircraft. The company is reportedly backed by Geely and anchors Chengdu’s low-altitude mobility cluster. Tengdun builds intelligent drone systems for civil and industrial use. Yongxiang produces polysilicon, a core input for solar cells.

The new entries are less a regional story than a national one playing out in Chengdu. The low-altitude economy was named in the 2024 government work report. Advanced unmanned systems and clean-energy supply chains have received explicit industrial guidance funding.

Sichuan’s broader cohort spans 10 sectors

Sichuan placed 11 companies on this year’s list. Ten are based in Chengdu, and one in Leshan.

The Chengdu cohort spans digital health (Medlinker), eVTOL (Aerofugia), intelligent drones (Tengdun), vaccines (WestVac Biopharma), cold-chain logistics (Xian Shenghuo), elevator advertising (Xinchao Media), animation (Coloroom Pictures), connected fitness (Fiture), trucking logistics (Juma), and tea retail (Shuyi Tealicious). Leshan-based Yongxiang manufactures polysilicon for the solar supply chain.

What the dispersion signals for investors

Chengdu’s 10-unicorn cluster marks a structural shift. The city now anchors a regional ecosystem spanning eVTOL, drones, biotech, animation, and AI-enabled consumer hardware.

Tier-1 dominance in private capital allocation may erode further as inland clusters mature and local government guidance funds professionalize. Suzhou’s 16 unicorns reflect its semiconductor and biotech base. Hefei’s 9 trace to its display, EV, and quantum-tech bets. Hangzhou’s 25 are anchored by its AI and platform-tech ecosystem.

Sector concentration in hard tech also raises average capital intensity per unicorn. That can lengthen path-to-exit timelines and reshape return expectations for late-stage RMB and USD funds alike.

Hurun’s projection for China clearing 500 unicorns within five years rests on the current pace holding. The composition matters more than the count. If semiconductors, AI, clean energy, and robotics keep dominating net additions, China’s unicorn pool will look less like Silicon Valley’s consumer-internet vintage and more like an industrial-policy portfolio.