Hy3 tops OpenRouter as Tencent’s AI architecture starts to deliver

Q1 2026 results show Hy3 preview leading global OpenRouter token usage, productivity agents posting 60-80% retention, and marketing services accelerating to 20% YoY growth.

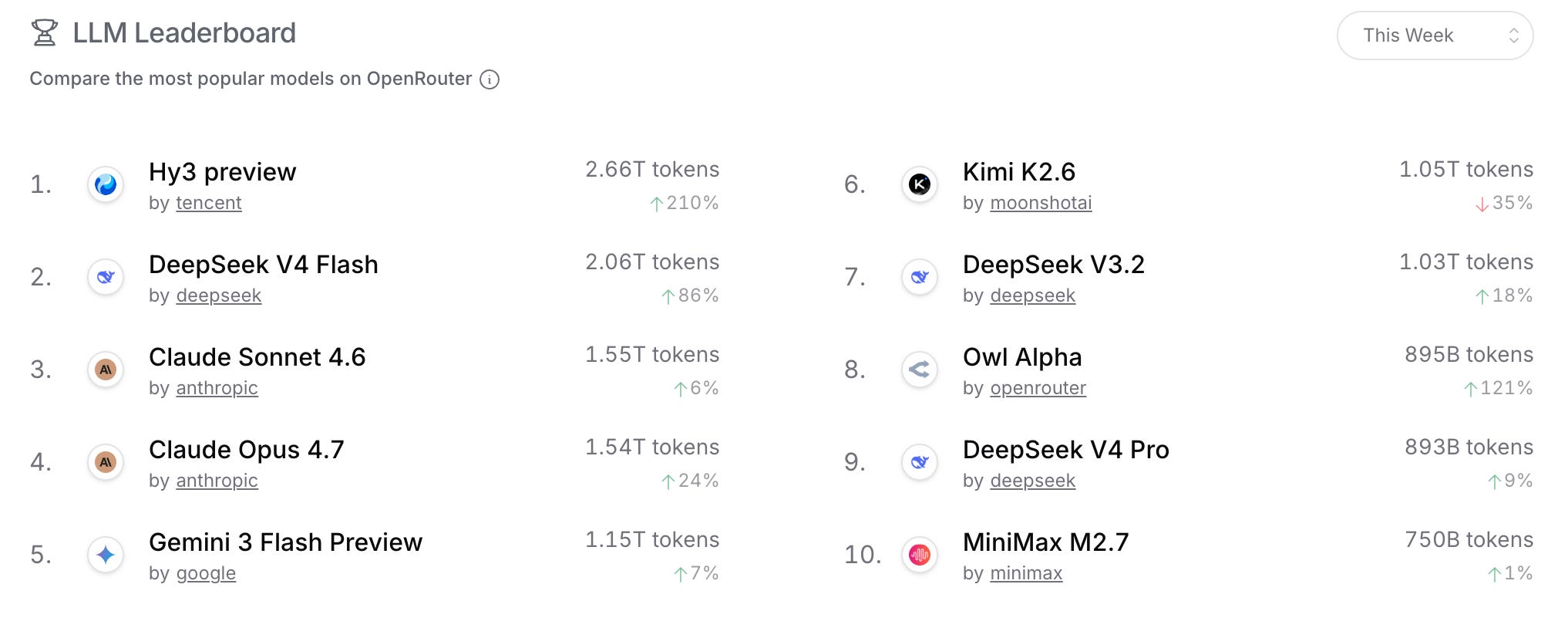

Hy3 preview topped OpenRouter at 7.7 trillion tokens since April 28, ahead of Kimi, Claude, DeepSeek, and Gemini.

Operating profit excluding new AI products grew 17% YoY to RMB84.4B, with margin expanding to 43.0%.

WorkBuddy leads China in productivity AI agents by DAU, with 80%+ retention among paying users.

Marketing services grew 20% YoY, accelerating from 17% in Q4 2025, with AIM+ powering approximately 30% of ad spend.

Tencent’s AI investment costs approximately 4.5ppt of operating margin, funded by RMB56.7B in quarterly free cash flow.

Tencent reported first-quarter 2026 results on May 13. Revenue reached RMB196.5B, up 9% YoY. Gross profit rose 11% YoY to RMB111.3B. For the first time, Tencent’s financial disclosures formally carve out “new AI products” as a separate cost center.

These products span Hy (the foundation large language model, "Hunyuan"), Yuanbao (consumer AI assistant), CodeBuddy (AI coding agent), WorkBuddy (enterprise productivity agent), and QClaw. The separation matters. It makes the cost of Tencent’s AI transition visible and measurable.

Tencent entered 2025 widely seen as a second-tier player at the foundation model layer. Moonshot’s Kimi, Alibaba’s Qwen series, and Baidu’s Ernie dominated analyst coverage of China’s large language model race. By April 2026, Hy3 preview had topped OpenRouter by token usage. The path from perceived laggard to lead took 12 months and a full rebuild of the model team.

Hy3 preview leads OpenRouter, rewriting the laggard narrative

Hy3 preview accumulated 7.7 trillion tokens on OpenRouter between April 23 and May 12, according to Tencent’s Q1 2026 results presentation.

The next closest model was Kimi K2.6 at 5.0 trillion tokens. Claude Sonnet 4.6 ranked third at 4.0 trillion. Claude Opus 4.7 registered 3.4 trillion. Gemini 3 Flash Preview reached 3.0 trillion. DeepSeek V3.2 placed sixth at 2.7 trillion.

Hy3 preview’s lead over Kimi K2.6 is 54% by cumulative token count in that window. OpenRouter routes developer traffic across multiple model providers, making token usage a direct proxy for developer adoption rather than self-reported benchmarks.

The model was built on comprehensively rebuilt infrastructure. Tencent rebuilt and re-staffed its foundation model team over the prior six months, bringing in what management described as LLM-native researchers and engineers.

Management characterised the new team as young, energetic, and cohesive. Pre-training, reinforcement learning, and evaluation systems were each rebuilt from scratch. Evaluation criteria shifted away from widely-gamed benchmarks toward real-world use cases and out-of-distribution tests, including unseen PhD qualifying exams from Tsinghua and Princeton.

Hy3 preview has been deployed across 131 internal Tencent products, including Yuanbao, QQ, WorkBuddy, and Tencent News.

The internal deployment creates a closed-loop feedback system: real-world product usage generates signal that informs iterative improvement. No external model provider can replicate that pipeline at this scale within a single company’s ecosystem.

The caveat is material. Hy3 is a smaller-parameter preview model. Tencent’s management acknowledged it is “just the first step.” The next milestone is scaling to a larger parameter model, leveraging the infrastructure and data learnings accumulated from Hy3. No public benchmark exists for the larger model.

Productivity agents are the first real test of AI monetization

Tencent’s agentic AI layer comprises three products. CodeBuddy handles AI code generation. WorkBuddy operates productivity software with higher security and controllability than general computer-use agents. Claws is an open-sourced general computer-use agent that interacts with the web and real-world infrastructure.

WorkBuddy is the most-used productivity AI agent service in China by DAU, according to Tencent. The claim is self-reported and comparable DAU data from competitors is not publicly available. The retention metrics are more informative. Among active users, CodeBuddy and WorkBuddy achieve 60%+ retention. Among paying users, that figure rises above 80%.

High retention among paying users signals genuine productivity value rather than novelty-driven engagement. Users who commit financially tend to churn unless workflows develop dependency on the tool. An 80%+ rate at this stage of the adoption cycle suggests that dependency formation is underway.

The agent monetization flywheel is beginning to operate. High-frequency agent usage enables Tencent to identify complementary services, deploy them, and deepen the user relationship. This expands agent utility for enterprise and prosumer users. As tasks grow more complex, paying user conversion increases. The downstream effect is accelerating token consumption on Tencent Cloud.

Tencent noted “rapid growth in token usage on Tencent Cloud in recent weeks” without disclosing specific figures. The agent-to-cloud revenue link is forming. Precise disclosure of token revenue contribution is a metric to watch in subsequent quarters.

The AI margin drag is quantified and contained

Q1 2026 is the first quarter investors can measure the direct cost of Tencent’s AI push. The arithmetic is clear.

Non-IFRS operating profit excluding new AI products grew 17% YoY to RMB84.4B. Non-IFRS operating margin excluding new AI products reached 43.0%, up from 39.9% a year earlier. Including new AI products, operating profit grew 9% YoY to RMB75.6B. Operating margin held stable at 38.5%.

The gap is approximately 4.5 percentage points of margin. The figure represents the current quarterly cost of Tencent’s AI product investment, expressed as forgone operating profit.

Selling and marketing expenses grew 47% YoY to RMB11.3B, driven by AI product promotion. Research and development costs rose 20% YoY to RMB22.6B. Capital expenditure reached RMB31.9B, up 16% YoY. Despite that spending, free cash flow grew 20% YoY to RMB56.7B. Net cash position rose 63% YoY to RMB146.9B.

The free cash flow figure is strategically significant. The core business generates sufficient cash to fund the AI build while maintaining share buybacks. Tencent repurchased approximately 12.7 million shares for a consideration of approximately HKD7.6B during Q1 2026.

The margin drag will likely widen before it narrows. The larger-parameter Hy model is in active development. Agent monetization is early. Infrastructure investment is ongoing. Investors should treat the current 4.5ppt drag as a floor rather than a ceiling.

Marketing services accelerated, validating AI-improved ad targeting

Marketing services revenue grew 20% YoY to RMB38.2B in Q1 2026, accelerating from 17% YoY growth in Q4 2025. The driver is a combination of improved AI-driven ad recommendation models and expansion of closed-loop commerce within the Weixin ecosystem.

AIM+, Tencent’s automated campaign management solution, powered approximately 30% of total marketing services advertiser spending in Q1 2026. The tool has gained traction specifically among mini game, mini drama, and Mini Shops advertisers, where closed-loop attribution is most direct.

Video Accounts’ total time spent grew over 20% YoY. Ad impressions grew rapidly as both total time spent and ad load increased. A new instant-play ad format for mini games embeds native gameplay inside the ad unit. This eliminates redirections and improves conversion rates for mini game developers.

Weixin Search query volume increased over 25% YoY, driven by LLM-powered ranking. The increase signals AI improvements to the search product are translating into measurable user behavior change, not just backend efficiency gains.

Marketing services at RMB38.2B is now the fastest-growing major segment. The AI-improved ad engine is subsidizing the AI build. The self-funding loop Tencent’s architecture requires is now active: better models improve ad targeting, ad revenue funds model development, and the cycle reinforces itself.

Tencent’s architecture differs from Alibaba and Baidu

Alibaba’s approach is cloud-infrastructure-first: Qwen models anchor the Alibaba Cloud value proposition and drive enterprise cloud migration. Baidu’s approach is vertical-first: Ernie is embedded into search, autonomous driving, and maps.

Tencent’s approach is distribution-layer-first: AI agents run on Weixin, QQ, WeCom, QQ Browser, and Yuanbao, with users interacting through familiar surfaces rather than new destinations.

Combined MAU of Weixin and WeChat reached 1.43B, up 2% YoY. The installed base is a structural advantage at the agent distribution layer. Users do not need to learn a new interface to access Tencent’s AI.

The Mini Programs ecosystem is a moat specific to Tencent. Over time, Mini Programs code can evolve into AI Skills: pre-built, context-aware tools deployable by agents within Weixin. Brand merchants on Mini Shops more than tripled their GMV YoY in Q1 2026. Mini Shops eCommerce transaction fees contributed to Business Services revenue growth of 20% YoY.

Tencent Cloud’s international revenue grew over 40% YoY, with global footprint spanning 65 Availability Zones. AI-related demand contributed to growth across GPU, CPU, and storage. At this growth rate, Tencent Cloud’s international operations are outpacing the domestic core. The enterprise AI agent proposition is gaining traction in markets outside China.

The distinction between the three Chinese tech giants’ AI architectures carries investment implications. Alibaba’s returns will be concentrated in cloud billings. Baidu’s will be concentrated in vertical monetization. Tencent’s will be concentrated in agent-layer activity across the existing user base. Q1 2026 results offer the first hard data on which architecture is converting capability into commercial momentum.

Risks and signals to monitor

The Hy3 preview OpenRouter lead warrants scrutiny on three fronts.

First, cumulative token usage on a developer routing platform does not directly translate to enterprise or consumer revenue. Developer adoption and commercial monetization are separate milestones.

Second, Hy3’s 54% lead over Kimi K2.6 may partly reflect novelty adoption from a new entrant. Third, the larger-parameter Hy model that Tencent is now developing has not been publicly benchmarked.

Revenue growth decelerated to 9% YoY from 13-15% across the three prior quarters. Domestic Games grew 6% YoY with Spring Festival timing distorting recognition. Fee-based VAS subscriptions declined 0.7% YoY to 266M, suggesting subscription monetization intensity within the platform is near a ceiling.

The fair value of listed investee shareholdings fell from RMB672.7B at year-end 2025 to RMB547.1B at March 31, 2026. The RMB125.6B decline in one quarter reflects broader market movements. It represents a meaningful erosion of Tencent’s investment portfolio value.

The 4.5ppt AI margin drag could widen materially if the larger Hy model requires significantly higher inference costs, or if productivity agent token consumption growth outpaces monetization conversion.

The architecture is functioning. The question is what comes next.

Tencent spent much of 2025 being assessed as a foundation model also-ran. Q1 2026 delivers three counters to that assessment: Hy3’s OpenRouter lead, WorkBuddy’s retention metrics, and 17% operating profit growth from the core business before AI costs.

None of these resolves whether the larger Hy model will hold its position. Nor does it confirm WorkBuddy’s DAU lead will survive pressure from Alibaba and ByteDance.

What Q1 2026 establishes is that the architecture is functioning. The distribution layer is distributing. The model is being used. The remaining question is whether the current trajectory sustains when the AI products are no longer excluded from the margin calculation.